European Long-Term Investment Funds (ELTIFs) In A Nutshell – Fund Management/ REITs

In A Nutshell – Fund Management/ REITs")

EH

ELVINGER HOSS PRUSSEN, société anonyme

Independent in structure and spirit, Elvinger Hoss Prussen guides clients on their most critical Luxembourg legal matters. Committed to excellence and creativity in legal practice, our firm delivers the best possible advice for businesses, institutions and entrepreneurs, playing a unique role in the development of Luxembourg as a financial centre.

Regulation (EU) 2015/760 on European long-term investment funds (ELTIF) has been amended by the revised ELTIF Regulation which is applicable since 10 January 2024.

Luxembourg

Finance and Banking

To print this article, all you need is to be registered or login on Mondaq.com.

1. ELTIF: distributing alternative strategies to

nonprofessional investors

Regulation (EU) 2015/760 on European long-term investment funds

(ELTIF) has been amended by the revised ELTIF Regulation which is

applicable since 10 January 2024.

On 25 October 2024, Commission Delegated Regulation (EU)

2024/2759 of 19 July 2024 supplementing the ELTIF Regulation (ELTIF

RTS) was published in the Official Journal of the European Union.

The ELTIF RTS enter into force on 26 October 2024.

On 25 October 2024, Commission Delegated Regulation (EU)

2024/2759 of 19 July 2024 supplementing the ELTIF Regulation (ELTIF

RTS) was published in the Official Journal of the European Union.

The ELTIF RTS enter into force on 26 October 2024.

These ‘democratized’ vehicles have been structured

mainly as ELTIFs or Luxembourg undertakings for collective

investment setup under part II of the Law of 2010 or the

combination of ELTIFs and Part II structures. The Part II fund is a

Luxembourg domestic AIF that may accept all types of investors,

including retail.

The ELTIF regime enables alternative investment fund managers to

market their AIFs in the EEA with a passport to retail investors.

Part II funds have been wellknown to investors beyond the EEA for

several decades.

An ELTIF may be set-up as a Part II fund (or a compartment

thereof) to release the full potential of its retail marketing

passport.

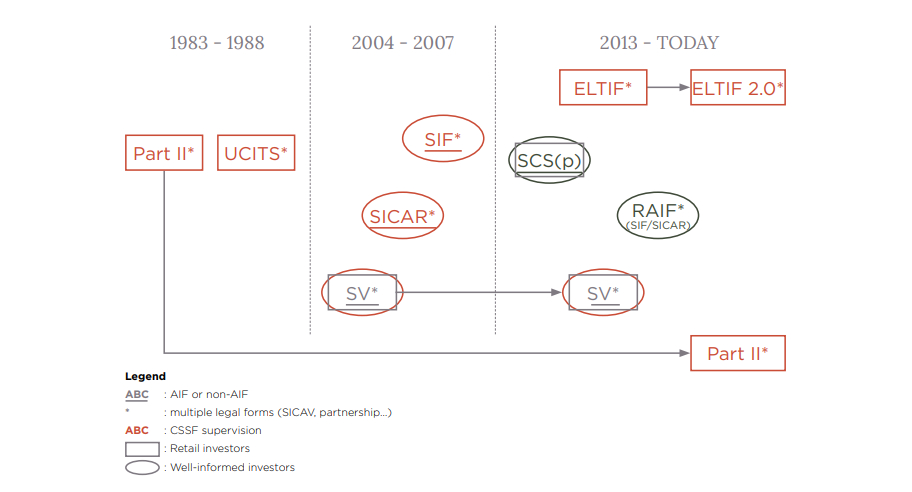

2.Overview of Luxembourg investment

vehicles

3. ELTIF key features

- Alternative investment fund (AIF) –

subject to AIFMD - Managed by an authorised AIFM – no

sub-threshold AIFM - Authorised and supervised by the financial regulator

(CSSF) – for compliance with ELTIF Regulation

aspects - Authorisation at the level of the sub-fund -

possible to add ELTIF sub-funds to an existing structure - EU marketing passport for professional and retail

investors – unique advantage for AIFs - Objective to facilitate the raising and channeling of

capital towards long-term investments in the real

economy

4. EU marketing passport

- The ELTIF Regulation is directly applicable in

all EU countries - Member states are not allowed to add

requirements in the field covered by the ELTIF Regulation

(art. 1 paragraph 3) - Notification procedure as per AIFMD for both

professional and retail investors

5. Eligible investors and distribution

| ELTIF | ELTIF – UCI Part II | ELTIF – RAIF, SIF or SICAR |

| ELIGIBLE INVESTORS | ||

|

|

|

| DISTRIBUTION | ||

|

|

|

| Delegating to /

appointing distributor(s) possible |

||

6. Marketing to retail investors – additional

requirements

Suitability test

- Obtaining information about retail investor (MIFID

II):

- their knowledge and experience in the investment field

- their financial situation

- their investment objective

- Providing statement on suitability (MIFID

II) - Express consent of investor possible in case

of negative statement - No MIFID II license required for AIFM

marketing directly

Depositary – additional requirements (application

of UCITS depositary regime):

- Entity authorised to act as depositary for UCITS (e.g. credit

institution) - No discharge of liability in the event of loss of financial

instruments held by a 3rd party - Liability of depositary cannot be excluded or limited

- Assets cannot be reused by depositary

PRIIPs Regulation

AIFMD

- Facilities: arrangement in host country(ies) to inform

investors, handle orders, liaise with regulator… (no physical

presence required)

7. ELTIF secondary market

- Listing of ELTIF possible

- Allowing free transfer of shares/units/interests is

mandatory

- subject to complying with regulatory requirements and

conditions set out in the prospectus

- subject to complying with regulatory requirements and

- Possibility to provide for full or partial matching of

transfer requests between existing and potential investors

as detailed in the ELTIF RTS

- subject to conditions set out in a detailed policy (role of

AIFM, timing, price, ratio, costs and fees)

- subject to conditions set out in a detailed policy (role of

8. Conditions for redemptions upon request

- ELTIFs can be structured as closed-ended vehicles or

open-ended vehicles - Redemptions are possible if provided for in the ELTIF

documentation - Timeframe: not during ramp-up OR not during minimum holding

period (except for feeder ELTIFs) - ELTIFs have to put in place a redemption

policy and liquidity management tools

compatible with the long-term investment strategy

- Anti-dilution liquidity management tool: ELTIF

manager may discretionarily select and implement at least one tool

among anti-dilution levies, swing pricing and redemption fees and

may select other tools under certain conditions

- Anti-dilution liquidity management tool: ELTIF

- Redemptions on pro rata basis if requests

exceed maximum % (possibility to foresee gating

provisions)

To view the full article click here

The content of this article is intended to provide a general

guide to the subject matter. Specialist advice should be sought

about your specific circumstances.

link

:max_bytes(150000):strip_icc()/Roi-5c4a640a34204da285b4ef1c98970be0.png "What Is Return on Investment (ROI) and How to Calculate It")