Are CEO successors more likely to implement environmentally responsible behavior? Empirical evidence from listed companies in China

Impression management theory

In sociopsychological research, impression management refers to the process by which an individual designs, modifies, and alters their behavior to control the impressions others form of them (Yuthas et al., 2002). In corporate strategy and management studies, impression management is considered a strategic tool, where a company actively improves and controls its image to achieve valuable objectives. It is also defined as “the control and manipulation of impressions conveyed to information users.” To gain resources and legitimacy from external stakeholders, companies often choose to engage in impression management to establish and maintain a favorable public image. Existing studies have found that companies use impression management to cope with declining performance, improve internal governance, and compete for scarce external resources and opportunities (Clatworthy and Jones, 2003). Even in the face of entrepreneurial failure, companies may use impression management strategies to mitigate the impact of negative events, such as reputation crises, caused by failure (Fisher et al., 2016). From the perspective of how impression management is manifested, research primarily analyzes its feasibility from the angle of information asymmetry, with positive information disclosure and corporate social responsibility receiving widespread attention (Chen et al., 2024; Hamza et al., 2023). Li et al. (2024b) found that companies use positive tones in their ESG reports to engage in impression management, misleading external investors’ perceptions of the company. Frutos-Bencze et al. (2024) showed that multinational companies use confident impression management strategies to attract the attention of various stakeholders in host countries when promoting innovation and implementing sustainable development goals.

This study extends the motivation for impression management from external stakeholders to the internal management level of the company. As a result of the board’s selection decision, a successor CEO’s continued appointment depends on further evaluation by the board. At this stage, the successor CEO, motivated by concerns about career stability, has a strong incentive to engage in impression management in the short-term to demonstrate their strategic decision-making and management capabilities to the board, gain internal recognition and respect, and secure a stable position within the company. Therefore, driven by the motivation for impression management, how the successor CEO views the company’s current environmental decisions becomes a key research question of great interest.

CEO succession in China’s institutional environment

For companies, CEO succession is a highly significant event. As the maker and implementer of corporate strategic decisions, the incoming CEO often brings substantial changes to the company’s prior strategy and development direction, and may even overturn previously designed strategic implementation models (Tao and Zhao, 2019). The highly competitive, market-driven environment has led to shorter CEO tenures, making CEO succession an important avenue for companies to address poor performance and shift strategic direction. Current research on CEO succession has extensively explored various aspects, including the driving factors behind CEO succession (Essman et al., 2021; Mooney et al., 2013), capital market reactions post-succession (Ballinger and Marcel, 2010; Cvijanovic et al., (2021)), and the impact of CEO succession on corporate strategy and decision-making (Schepker et al., 2017; Shaheen et al., (2023); Zhou, 2023).

In recent years, as the economic strength and visibility of Chinese-listed companies have continuously increased, CEO turnover has attracted more attention in both theoretical and practical fields. According to a survey on CEO turnover rates, in 2010, the global CEO turnover rate was 11.6%, while the rate in Chinese-listed companies was just 5.2%. However, within just four years, by 2014, the CEO turnover rate for Chinese-listed companies had skyrocketed to 15%, making it the highest in the world. The unique institutional characteristics of China provide an appropriate context for this study. In Chinese institutional and philosophical systems, the concept of “stability” holds great significance. From the governance ideologies historically promoted by ruling classes to the emphasis on the stability of land and climate in agricultural civilization, as well as the long-standing cultural tradition, “stability” has always been a central value. Driven by a strong pursuit of position stability, the successor CEO often exhibits a strong motivation for impression management during the board’s post-selection oversight phase. By demonstrating superior management and decision-making capabilities to the board, the successor CEO seeks to earn the respect of company members and establish their position within the company, avoiding the risk of career setbacks due to short-term decision-making mistakes.

CEO succession and corporate environmental responsibility (CER)

Impression management theory suggests that individuals in any organizational context desire to be positively viewed and recognized by others, and they take different actions in different situations to maintain their image (Graffin et al., 2011; Lee et al., 2020). The succession of a CEO involves a rigorous selection and evaluation process by the board, followed by a review and assessment to make decisions regarding dismissal or approval to ensure that the CEO’s professional capabilities align with the company’s internal and external environment and development goals (Liu, 2020; Zhang and Rajagopalan, 2004). In other words, a successor CEO, in the short-term, not only faces the pressure of gaining a competitive advantage and improving corporate performance but also the “career concerns” arising from board oversight and evaluation. This undoubtedly forces the CEO to make choices and trade-offs regarding resource allocation under the constraints of corporate resources. According to impression management theory, the successor CEO, in order to prove their managerial capabilities, gain the trust and recognition of the board, and eliminate the threat of departure, will choose strategic decisions that enhance their position stability. They will invest resources in strategies that yield quick results to achieve short-term performance improvements (Driver, Guedes, 2017; Liu et al., 2021). Simultaneously, the “quick win” hypothesis suggests that successor CEOs, driven by “quick win” motives, will opt for decisions that favor their interests, consciously directing resources towards actions that align with their short-term goals to establish authority and demonstrate capability (Chen et al., 2015).

Fulfilling environmental responsibilities often represents a high investment in the company’s limited resources (Li et al., 2020; Xu et al., 2018). Compared to investments in highly visible actions such as increasing product promotions or enhancing quality and safety measures, investments in improving pollution management or enhancing environmental management technologies have longer investment cycles. Additionally, for stakeholders such as shareholders, environmental measures are often seen as abstract information, with short-term returns not immediately apparent, making it difficult for the successor CEO to demonstrate managerial competence. Although fulfilling environmental responsibility can be beneficial in the long-term by gaining stakeholder recognition, enhancing corporate reputation, strengthening value creation, and improving the CEO’s image within the board (Liu, 2020; Gong et al., 2018), the successor CEO, due to limited authority and the short-sighted “quick win” mindset at the early stage of their tenure, tends to be more conservative and cautious in strategic decision-making. They are more likely to choose projects with high short-term returns and reduce long-term investments (Liu, 2023). Additionally, existing research has shown that CEOs may also exhibit a “strategic motivation” to fulfill environmental responsibility at the cost of shareholder interests and corporate value, thereby overspending on environmental responsibility to improve their personal reputation or gain personal benefits (Barnea and Rubin, 2010). If a successor CEO chooses to fulfill CER, it not only means abandoning some short-term strategies that yield quick results but also exposes them to accusations of opportunism and moral hazard (Ballinger and Marcel, 2010; Intintoli et al., 2014), which may result in decreased financial performance and shareholder losses. Consequently, the successor CEO would struggle to prove their competence to the board and shareholders in the short-term, establish authority in front of employees, and gain the recognition of the board and investors, all while failing to use “quick wins” to alleviate the threat of departure and solidify their position (Call et al., 2009). Therefore, under the influence of impression management and “quick win” motives, the successor CEO’s motivation to fulfill CER is weakened, and they are more likely to opt for other decisions to maintain position stability and avoid the threat of departure. Based on the above discussion, the following hypothesis is proposed:

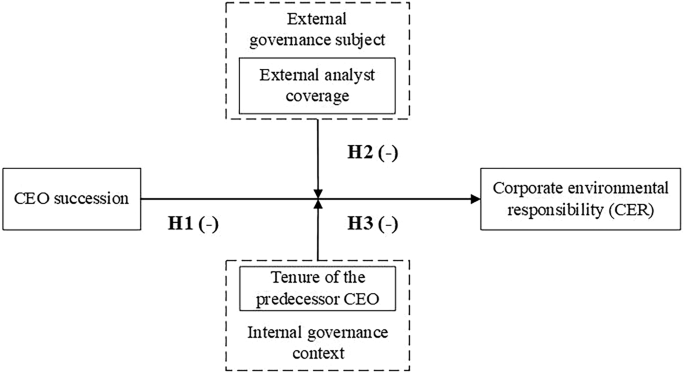

Hypothesis 1: CEO succession has a negative impact on CER.

The moderating effect of external analyst coverage

External analysts are professionals with securities investment consulting qualifications who provide investors with research reports and investment recommendations for publicly listed companies. They serve as a bridge for information transmission in the capital market, offering valuable professional insights (Jens, 2017). With their specialized knowledge and skills, external analysts gather, process, and disseminate information about listed companies. By doing so, they expand the range of information available to investors, increase corporate exposure and visibility, and act as an external governance mechanism for monitoring corporate management. Existing research suggests that external analysts, through monitoring internal management, can effectively reduce the information asymmetry between companies and investors, improve the efficiency of market resource allocation (An et al., 2020), reduce earnings management (Sun, 2009), and curb moral hazard and opportunistic behavior by controlling shareholders and management (Anantharaman and Zhang, 2011). We propose that external analyst attention will strengthen the negative impact of CEO succession on CER, for the following reasons:

External analyst attention brings greater exposure to the company but also increases the scrutiny of the successor CEO (Connelly et al., 2016). The successor CEO faces not only the potential threat of a change in position from the board but also the psychological uncertainty from external market investors and analysts, who may become more inclined to negatively evaluate the successor CEO’s early performance due to concerns about the unclear future prospects following the CEO change (Jung, 2017). This increases the external attention on the successor CEO, and such external evaluations significantly influence the board’s decisions regarding dismissal or retention. Under these internal and external pressures, the successor CEO, considering their limited power and high position uncertainty (Ballinger and Marcel, 2010), experiences a stronger impression management motive, with a greater desire to achieve “quick wins” in the short-term to demonstrate capability.

Given that fulfilling environmental responsibilities demands a significant allocation of resources, has slow short-term returns, and is often seen as yielding less immediate benefits, it may also attract suspicion and criticism from external market investors and analysts due to the potential for “strategic motivations” aimed at personal gain. As a result, to gain recognition for their capabilities and alleviate negative external evaluations, the successor CEO is likely to “appease” external market investors and analysts by reducing resource allocation to environmental initiatives and minimizing CER. Instead, they would prioritize short-term high-return investments to improve corporate performance. This approach sends a signal to both internal and external stakeholders that the successor CEO is capable of managing the company, helps dissipate doubts among external investors and analysts, boosts confidence in the successor, and reduces negative judgments and reports. Consequently, this may lead to a relaxation of board-level oversight and alleviate the successor CEO’s “career concerns,” helping to maintain position stability (Marquis and Tilcsik, 2013). Based on the above discussion, we propose the following hypothesis:

Hypothesis 2: External analyst coverage strengthens the negative impact of CEO succession on CER.

The moderating effect of predecessor CEO tenure

We hypothesize that the tenure of the predecessor CEO will also strengthen the negative impact of CEO succession on CER. The reasoning is as follows: First if the successor CEO allocates more resources to environmental responsibility, it does not simply mean eliminating high-energy, high-pollution fixed assets, developing and purchasing clean production equipment, or increasing costs for pollution control and management. The key issue is that a long-tenured predecessor CEO tends to create a relatively fixed set of interest groups and structures due to their decision-making characteristics (Liu and Atinc, 2021). To ensure the proper execution of environmental responsibility, the successor CEO must break away from the behavioral routines and structural patterns established by the predecessor CEO, integrating the relevant responsible departments. In the short-term, this will demand significant effort and disrupt the established interest groups and patterns within the company, increasing resistance to inter-departmental collaboration and potentially causing internal conflicts and power struggles within the executive team (Li et al., 2009; Ballinger and Marcel, 2010). Ultimately, this may introduce volatility and risk to the company’s smooth development, reducing the board’s risk tolerance and intensifying the successor CEO’s threat of dismissal and “career concerns”.

Second, the tenure of the predecessor CEO directly influences the board’s risk sensitivity. As the originator and executor of previous strategic decisions, the background and perspectives of the predecessor CEO significantly impact the company’s future development and resource allocation direction. As the predecessor CEO’s tenure lengthens, the board becomes more familiar with their performance, which reduces the need for supervision and the intensity of oversight (Deng and Lin, 2014). When a long-tenured CEO leaves, the resulting short-term disruption in management and stagnation in strategic direction raises the board’s perception of risk. This increased risk sensitivity, combined with uncertainty regarding the company’s future, is transferred to the successor CEO through intensified supervision and evaluation, as the board uses these measures to “ease” their own concerns (Karaevli and Zajac, 2013). Therefore, if the predecessor CEO’s tenure is long, the successor CEO will face greater difficulty in fulfilling environmental responsibilities and will be subject to more intense evaluation by the board. In this scenario, the successor CEO’s impression management motives are further strengthened, and they are more likely to pursue “quick wins” to improve short-term performance, alleviate “career concerns,” and reduce the threat of dismissal, ultimately decreasing their willingness to fulfill CER. Based on the above discussion, we propose the following hypothesis:

Hypothesis 3: The tenure of the predecessor CEO will strengthen the negative impact of CEO succession on CER.

The overall study model is shown in Fig. 1.

link